20Sep1:12 pmEST

What if it is the Pause Which Refreshes the Bond Selloff?

As we know, Jerome Powell is more than capable of being bullied into a corner. Case in point: Back in 2018 Powell was a brand new Fed Chair. He came out swinging with rate hikes and generally adopting a hard money approach, especially compared to the Bernanke and Yellen years. Then-President Trump ultimately made a point to publicly turn the heat up on Powell continually, including a barrage of social media tweets as stocks sold off aggressively in late-2018.

Ultimately, Powell caved in a rather pronounced way, and stocks rallied as rates fell for several quarters thereafter.

Fast-forward to the last forty-eight hours in front of the FOMC at the bottom of the hour today, and we have seen constant Janet Yellen and Nick Timiraos remarks and media appearances.

Now, it is uncertain if they are all on the same page. But, boy, Yellen and Timiraos seemed rather cocksure that The Fed need not raise rates today. And the market agrees, expecting a 99% chance or so as I write this of a pause.

But that raises the real issue at hand: Will the pause by Powell today necessarily mean a rally in both stocks and bonds?

For now, let us just focus on bonds. On the surface, a pause *should* put a top in rates and be a green light to dip back into bonds.

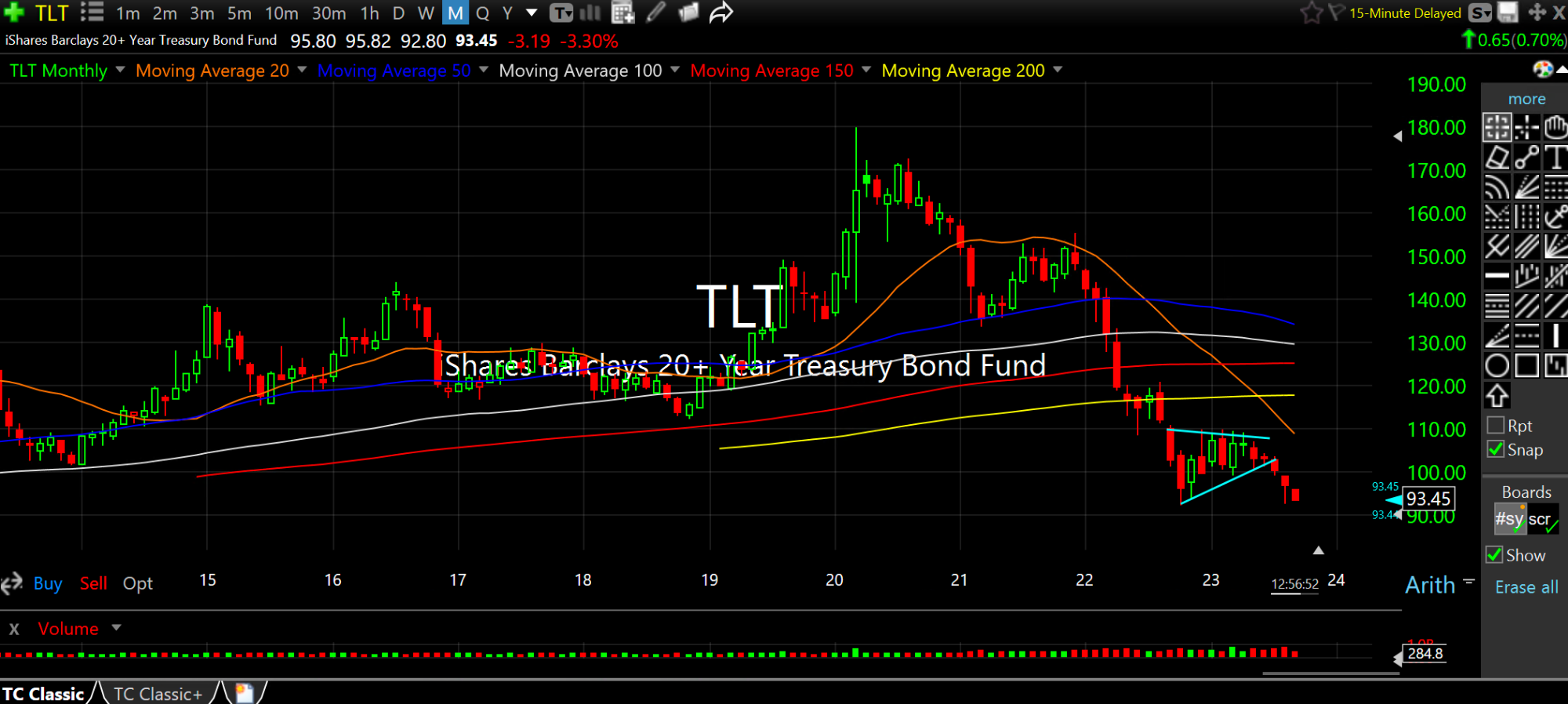

However, what if, perchance, the pause ignites a further selloff in bonds as rates rise? Recall that the prevailing trend in Treasuries, below on the TLT monthly chart, is firmly lower. It is often said that big news events tend to resolve in favor of the prevailing trend.

Next, if The Fed is not being sufficiently restrictive with rates currently, it stands to reason that pausing here will only allow a resilient economy to keep on chugging, which means rates actually should be higher and that will be good reason for a further move from here.

Even with a pause, The Fed likely continues with quantitative tightening and not signaling a rate cut anytime soon. A "hawkish hold" as they say.

But what matters most to me, as has all year, is that downtrend in Treasuries amid what is still a new, secular regime change to higher for longer rates after forty-plus years of disinflation and falling rates.