18Mar3:28 pmEST

The Last of the Growthicans

The latest FOMC came and went, with Fed Chair Powell's presser just having wrapped up. Despite being adamant about continuing in his role if Kevin Warsh's nomination runs into issues, he also seemed befuddled about verbalizing that inflation has, in fact, been above The Fed's 2% target for five years and running. He uttered that statement a few times, and my read was that he himself knew just how ridiculous this whole situation has been, through no fault of his own.

Indeed, The Fed ought to have kept raising rates back in 2022 and certainly should not have cut rates in 2024-2025--I have been consistent in my views on this matter.

Unfortunately, we will likely pay the price as a society under the guise of Iran (short-term versus long-term) and other assorted excuses. In reality, there has always been a certain inevitability that we would see persistent inflation given The Fed's absurd policies over the decades and especially since 2008.

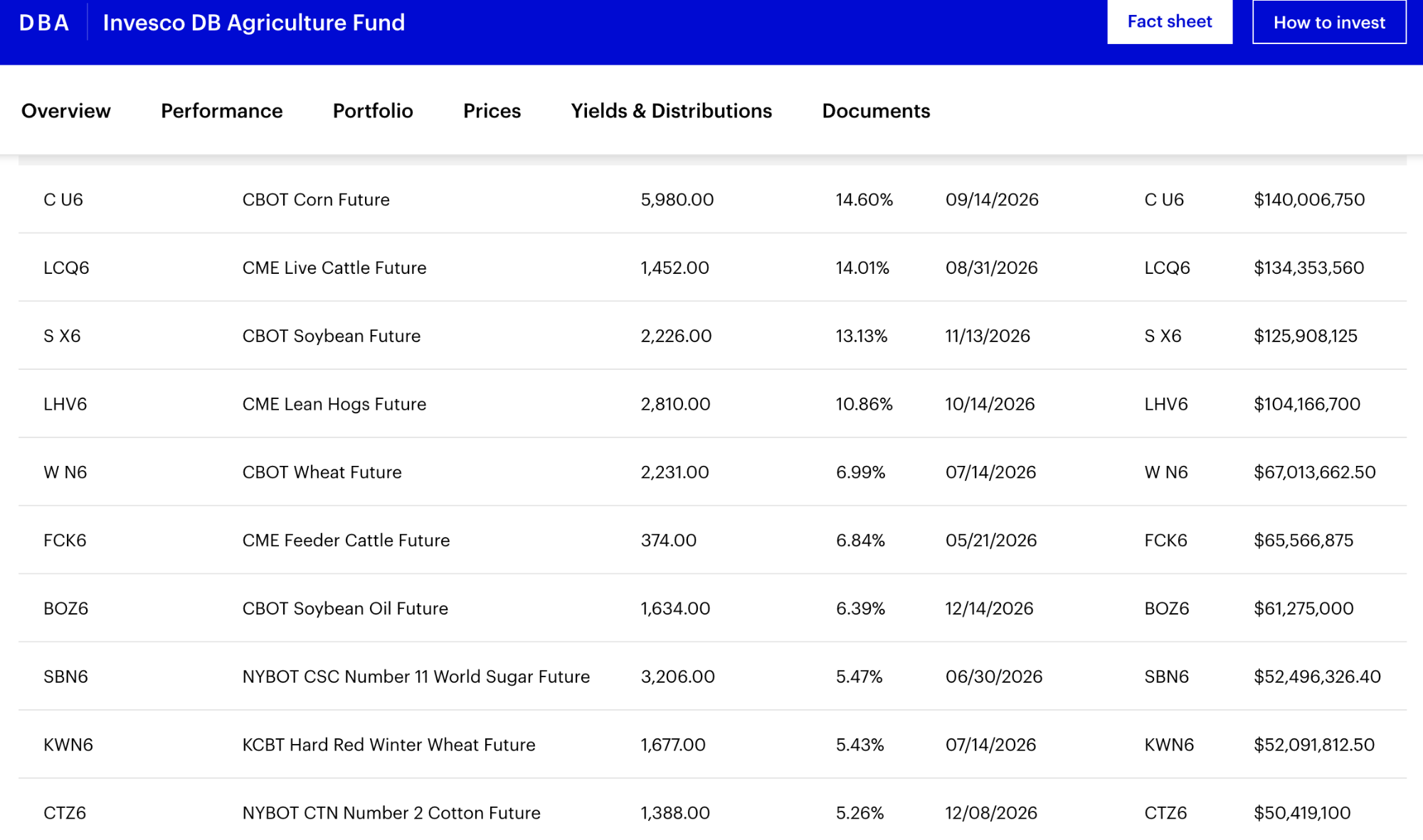

On that note, DBA, the ETF for a basket of soft commodities, is reminding us that the Strait of Hormuz is not just about oil at all. Various softs, listed immediately below, are in the DBA and the ETF daily chart, below that, is coiled up and strong today. Again, short-term effects of Iran, but long-term inevitability with The Fed.

Elsewhere, Micron reports tonight. MU and Sandisk seem like the last of the growth stocks thriving, as most of the Magnificent 7 (plus HOOD PLTR etc.) have either broken down below their 200-day moving averages or seem on the cusp of doing so (AAPL NVDA).

MU has a tall task tonight and a high bar to exceed estimates for memory AI.