07Apr3:27 pmEST

You Can Change the Route But Not the Destination

"You can change the route but not the destination," is a saying some of the Wall Street old timers used to throw around throughout 2008, especially in March of that year after the Bear Stearns fiasco (they, infamously, wound up getting taken over by JPM at $2 per share) led to a multi-month bear market rally. I am reminded of that phrase as the market whips around today on alternating headlines of hope that talks remain alive (despite Iranian denials) for a deal by Trump's 8pm EST deadline tonight.

On the one hand, the Dow, S&P, and Nasdaq all remain below their respective 200-day moving averages. But on the other hand, there is a clear continent of market players who do not want to miss on out that "TACO" rally we have seen so many times, where Trump brags about a last-minute deal or progress on a deal to stave off the outcome of American becoming (even more of) a bellicose nation. Hence, intraday and overnight dips have been bought, but also have not yielded much in upside.

Given the high stakes nature and insinuation of nukes, it is easy to overlook the next few days of major macroeconomic events. Tomorrow we have the FOMC Minutes, followed by the PCE, GDP, and CPI on Thursday and Friday. I suspect the Minutes may be more hawkish than some expect. And the PCE/CPI may start to show the early effects of gas prices surging.

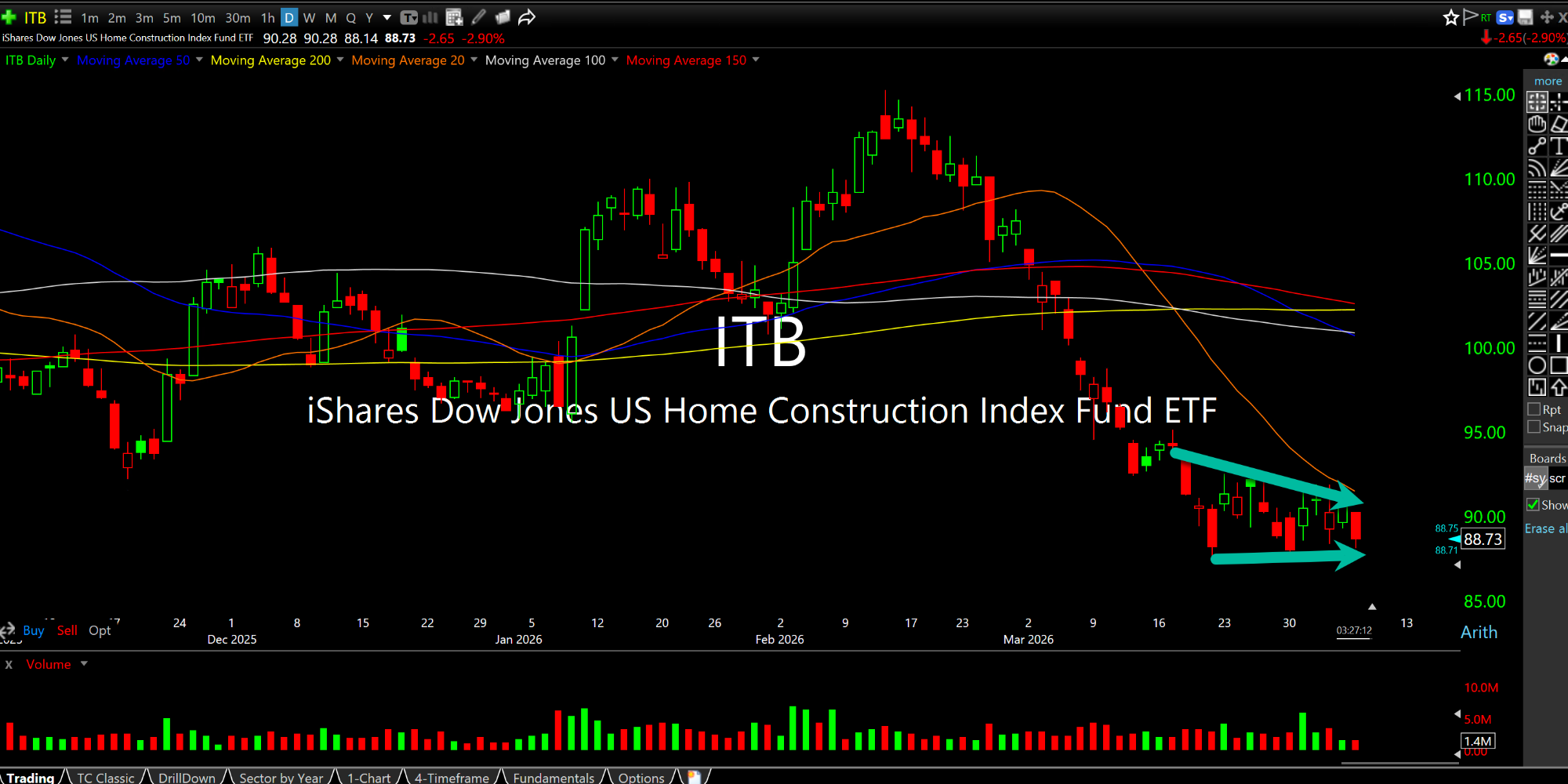

But housing's weakness continues to hide in the shadows of Iran. On the ITB ETF you can see one of the weaker sectors of late, failing to bounce even from oversold conditions. With a declining 200-day moving average well above price, the market is finally suggesting that the seemingly unstoppable centerpiece of the U.S. economy is long in the tooth and ripe for an overdue unwind further.

Believe me when I tell you that The Fed and federal government have tried for years and years to change the route. And they did. But they cannot change the destination for housing.