27Apr3:16 pmEST

Going Global to Undermine the Oil Bear Case

One of the more popular arguments oil bears are making right now to justify crude oil not quite super-spiking is that the wisdom of the market is accounting for "demand destruction," be it from China and/or the world at-large. This argument seeks to squash any notion of, hypothetically speaking, government intervention in the front month contract for WTI crude oil to suppress it as a means to contain the fallout from the ongoing Strait of Hormuz disruptions. Hence, we have the continued discrepancy between WTI futures and physical Brent crude oil prices, (or "Dated Brent").

However, when we examine the demand destruction view, we currently have two opposing forces to it in markets.

First and foremost, rates across the curve are higher again today, with the 10-Year Note failing to breach 4.2%, below, since the melt-up in equities began just under a month ago. Now, the 10-Year is threatening an upside break of 4.34%-4.35% to resume the prior uptrend since the Iran War broke out in late-February. This is not exactly the stuff out of which deflationary "demand destruction" is made.

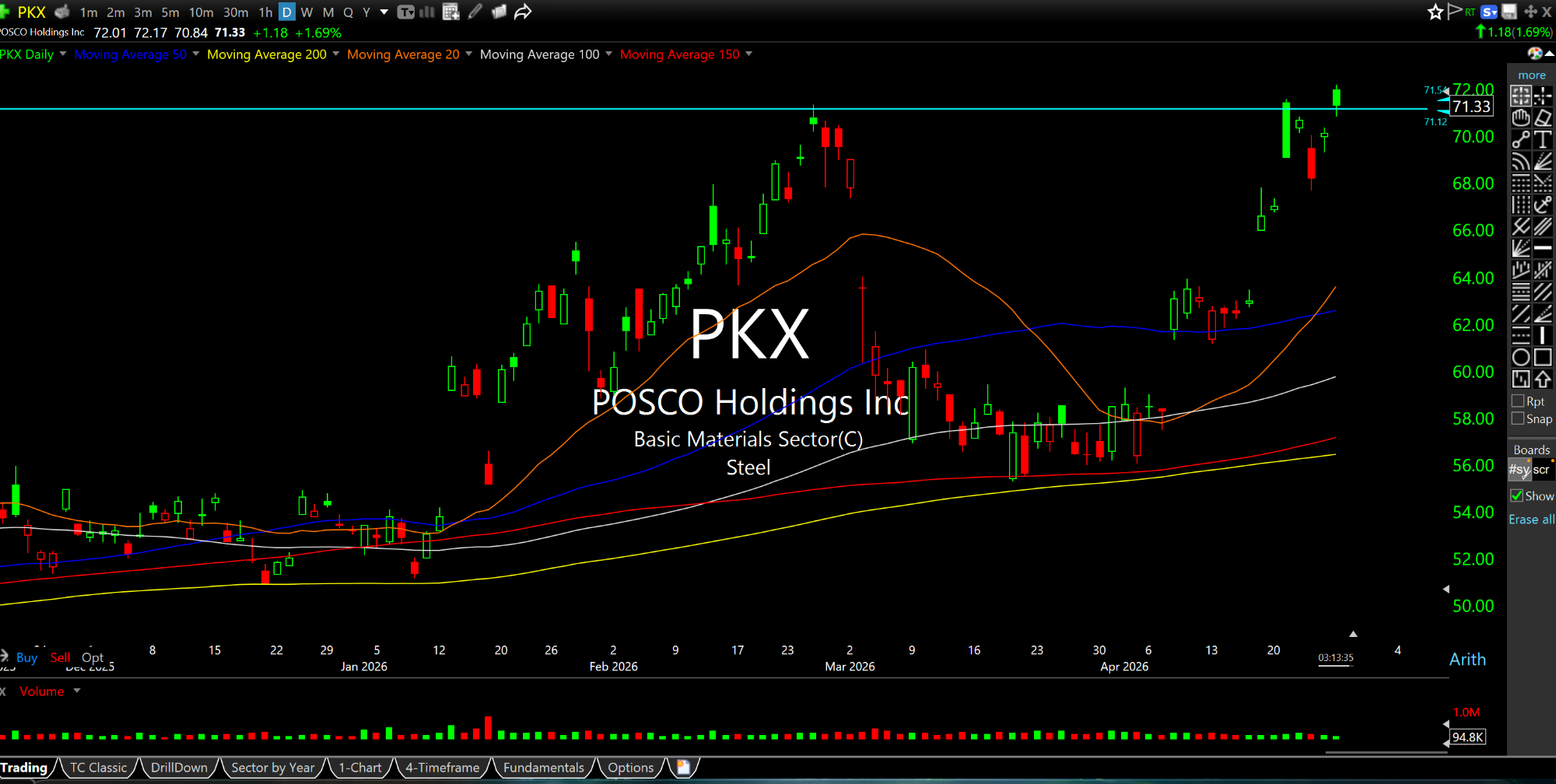

Secondly, the global non-precious materials miners are acting impressively. Specifically, the likes of BHP VALE, as well as South Korean steelmaker PKX and RIO, respectively below on their strong, clean daily charts. Again, this is not likely to occur in an environment with potent demand destruction to the point where it would trump (no pun intended) the greatest oil supply shock in at least fifty years, if not ever.

Simply put, each passing day that the Strait of Hormuz remains significantly disrupted pressures markets to face reality for a confrontation it has clearly been postponing, heretofore. Both the bond market and the biggest global base miners vehemently disagree with oil bears and their misguided arguments.

Afternoon Update 04/24/26 {V... The Test Almost Always Comes...