14Jul3:18 pmEST

Deflation in Mirror is Smaller Than it Appears

As you would expect we have the White House and bulls/doves at-large feeling their oats over this morning's cold CPI print.

Without question, the hard correction in oil, gasoline, and most commodities since May affected the print, leading many to declare that inflation has, once again, been conquered and we can expect much lower gas prices from here.

However, the issue we raised with Members both last evening as a preview for the CPI and again today is whether the market would, in effect, "look through" a cold CPI print and eventually arrive at the conclusion that this would be a blip within the context of a larger inflationary regime.

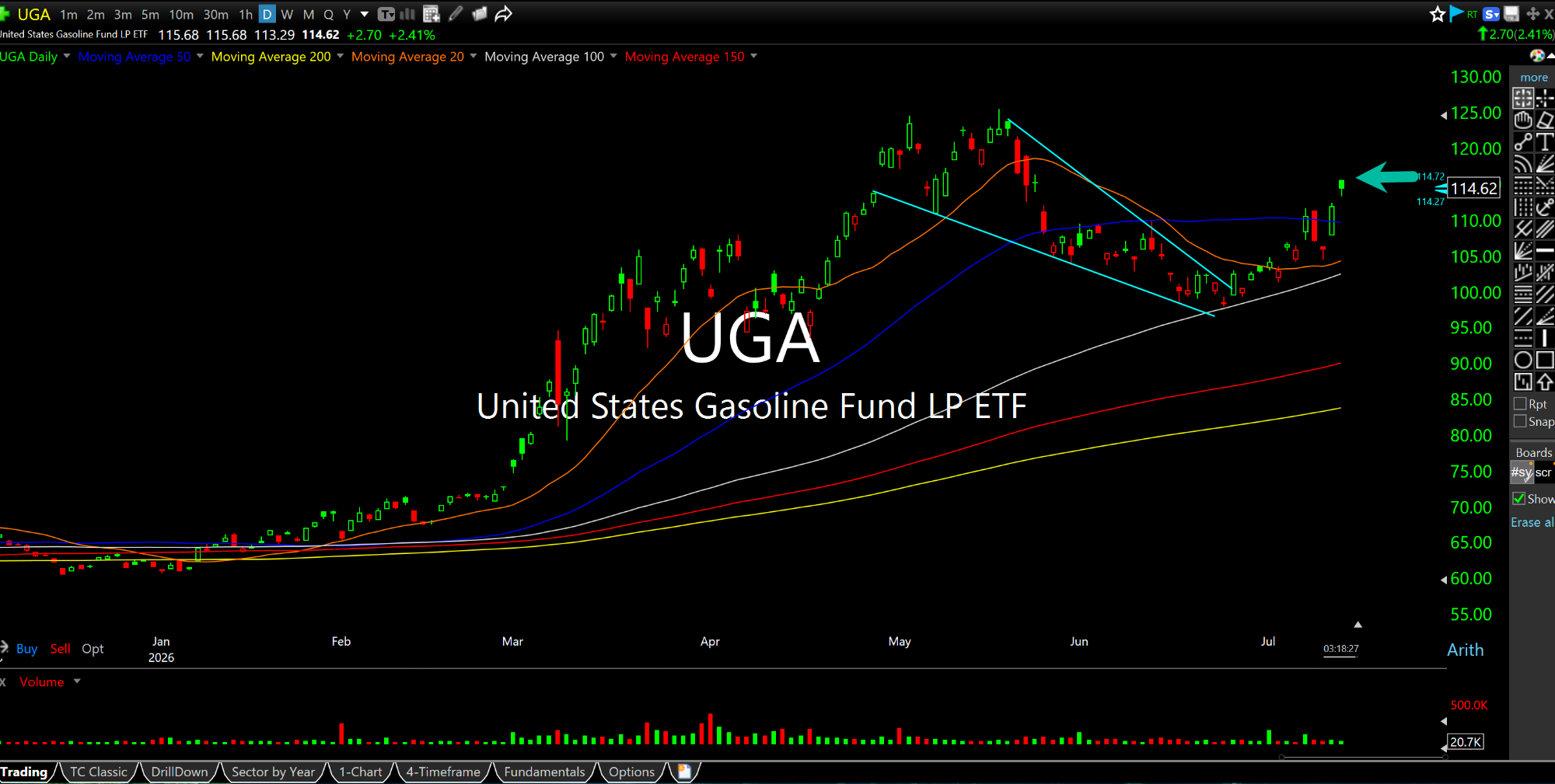

And as you can see on the updated UGA (ETF for gasoline futures, rolling nationwide) daily chart, below, gasoline (and crude oil) are snapping back today and recouping a fair amount of the losses in the May/June correction. In addition, bond prices are staging a rather pedestrian bounce off the cold CPI rating, with rates on the 10-Year well off session lows.

Thus, if it were true that this morning's CPI were a sign of sustained disinflation or even deflation from here, several asset classes seem less than convinced about it.

While equities are bouncing back today, with semis and the Nasdaq leading, we still see largely sideways patterns since May for both the QQQ and SMH as we embark on the summer earnings season. Given the IBM carnage today, down 24% as I write this, coupled with New York State's moratorium on data centers, the largest semis and AI plays had better come in above the highest whisper numbers this earnings season.