07May3:32 pmEST

Much Hype, But No Hyperbole Here

The reversal down in bonds (and thus reversal up in rates) earlier in today's session was one of the main things we noted with Members this morning. Simply put, we wanted to see if equities would finally buckle a bit and respond to stubborn oil and gasoline as well as Treasuries struggling to hold much of a rally.

As we wind down today's session we now have the semiconductors down about 2%, which of course is barely a flesh wound compared to the historical melt-up. However, one has to start somewhere, especially as we head into more AI-related earnings tonight and the big jobs report tomorrow morning, followed by a new Fed Chair potentially taking over by the end of next week.

Indeed, there remains enough hype with AI and in this market overall to go around, despite some glaring sore spots like SHAK WHR earnings, two keys for a struggling consumer below the surface of the QQQ/SMH/SPY parabolas.

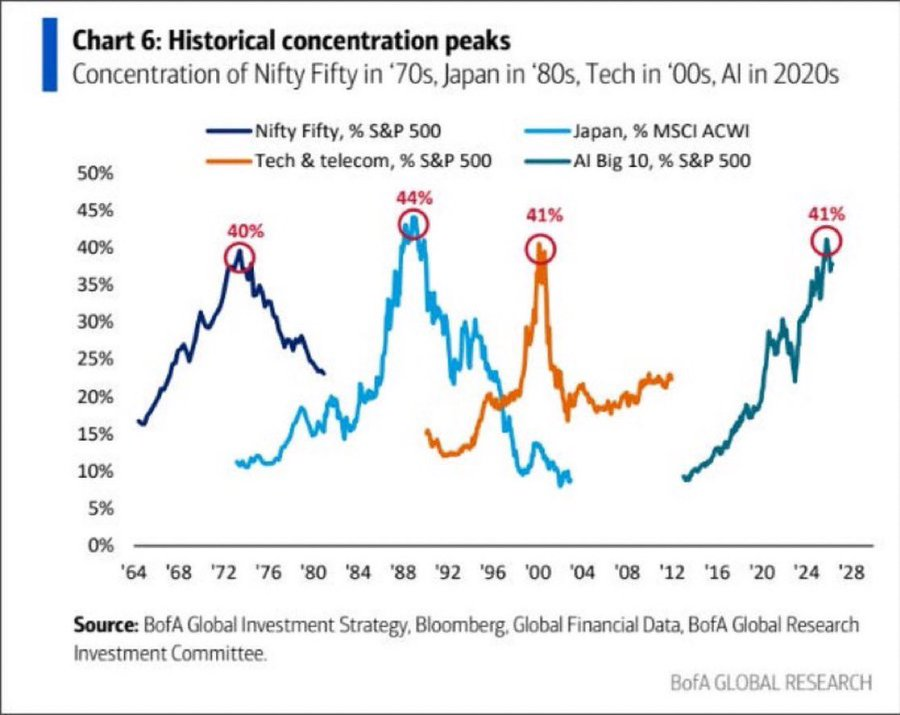

On that note, it is not hyperbole, despite what many are claiming, to compare today's AI bubble to prior bubble tops.

As evidence, consider the concentration risk, seen below on a chart I saw making the rounds on social media earlier this week, courtesy of BofA Global Research.

The 40%-plus concentration in the S&P 500 from AI names rivals the NIFTY FIFTY, Nikkei, and Dot-Com bubbles, objectively speaking. To counter with, "But they have earnings" is to ignore the same argument made in prior bubbles, especially near the tops--This is as bifurcated as bifurcated gets with everyone crowded in the biggest winners.